When it comes to negotiating settlements on private student loans, it pays to have an expert in your corner. Debt collectors have an information advantage during settlement negotiations, and many borrowers are doing it for the first time when they attempt to negotiate on their own. Some people get lucky and get a decent settlement, and get even luckier when they avoid potential pitfalls and issues that can arise during settlement execution.

Problems with Student Loan Settlements

However, there are many other instances where borrowers have paid funds for a settlement only to find out that it was misapplied, or even worse, they get a phone call from another collection agency claiming no knowledge of the settlement amount they paid. Still other issues involve improper credit reporting. A recent client of mine had an improper notation on his credit report – after settlement, it still said that the account was charged off, and the balance owed was showing as the amount that was saved in settlement. The account should have been reporting as “settled for less than the full balance” with a zero balance showing. After a couple of phone calls and a polite but serious threat that we were going to file a certain type of regulatory complaint if it was not fixed, the lender promptly updated their credit reporting.

There can be pitfalls associated with hiring a professional debt negotiator or a debt settlement company as well. The industry is highly regulated, and upfront fees are completely prohibited due to the actions of scammers and unethical companies that thrived during the Recession, when credit card defaults skyrocketed. Getting involved with an unscrupulous debt settlement company can make a borrower’s problems even worse. So it’s understandable that people want to try to do it on their own. How hard can it be, they ask. Then they get on the phone with a debt collector who spends 8-10 hours a day, 5-6 days a week, honing their collection skills. It’s usually a mismatch.

The collector will get what they want, and the types of measures that we take with clients to ensure that settlements are properly documented are not high on a collector’s list of priorities. Their main priority is getting the payment in as fast as possible, in the easiest way for them. A debt collector will happily take a payment over the phone, via a clients’ personal checking account, without sending them a written offer first. Strike one, strike two, strike three. The stage is set for a potential settlement disaster since the client has no documentation and no proof of the settlement other than a one-line listing on their bank statement.

These types of issues don’t happen with every settlement, but they do happen enough that finance and debt advice message boards have tons of messages from people who are in a bind after they paid for a settlement without proper documentation and improper execution procedure. Borrowers who do this are basically putting all of their trust in the debt collector and the debt collection company to do everything right and not make any mistakes. Since the debt collection industry receives well over 100,000 complaints every year, trusting them completely without any documentation to fall back on is probably not the best idea. With the amount of money involved in settlements, gambling that everything will go smoothly without taking the proper precautions is like sitting down at a table of professional poker players and expecting to win a fortune. Unless you are a professional poker player yourself, there’s a good chance that the other players will use your inexperience to their advantage.

Even if the borrower gets lucky and doesn’t experience any of the potential pitfalls that litter the path to a successful settlement, they are probably going to get hard-balled by the debt collector into taking an offer that’s greater than the debt collector’s bottom line. When I negotiate for clients, it often involves many rounds of offers and counter-offers. Often times, I get inquiries from people who want to settle for a certain dollar amount, and that dollar amount is what they use as their opening offer when they try to negotiate on their own.

The debt collectors’ opening offer (or counter-offer if the borrower presents the opening offer) is likely to be much higher than the “basement” amount they are authorized to settle for. Their first and even second counter-offers may also be quite a bit higher than the optimum settlement that’s available. It’s not unusual for me to go 6 or more rounds of offers and counter offers with a debt collector. And even then, we may not have the offer that I want. I may have to hold firm on my final offer for a month or two, do a “freeze-out” with communications, or provide a budget workup that shows why the settlement I’m offering is the best my client can afford. Settlement negotiation is both an art and a science, and I use different tactics depending on the different obstacles and concessions I’m seeing from the opposing party. As my former martial arts teammate used to say, we’ll take “whatever comes down the river”. That means that we are well equipped to deal with any actions that the debt collector takes, and still achieve the outcome that we want by adjusting our strategy and counterattacks to their actions.

I received this email yesterday, from a borrower I had first spoken with in May for a free consultation:

Free Advice vs. Professional Services

There are several issues here. They want me to review some text from their settlement letters without sending me the full letters, and they also seem to assume that I would do this for free. I get these kinds of questions from time to time, and I suppose that because I offer free consultations that sometimes last 20-30 minutes, people occasionally assume that I can continue helping them for free if they decide to do it on their own. I believe in giving free advice when possible, but I can’t give away a crucial part of my core debt negotiation service.

It’s sort of like me going into an auto repair shop, getting a detailed rundown on how they would replace my rusty rear bumper, then, after attempting to do it myself, making a call to the auto repair shop asking them about specific instructions on the repair process when I get stuck. In debt negotiation, as in auto repair, it’s normal for people to want to get the best deal they can while spending the least amount of money, and I certainly don’t fault anyone for trying to do that.

But in the attempt to save money through a DIY effort, this person is actually losing money. Going back to the email, they say that they got a settlement for 55% of the balance on a Navient account. I’ve personally never settled a Navient account at higher than 45% of the balance. In many cases with recent defaults, I even get closer to the 40% range. Find out more about how to settle a private student loan with Navient here.

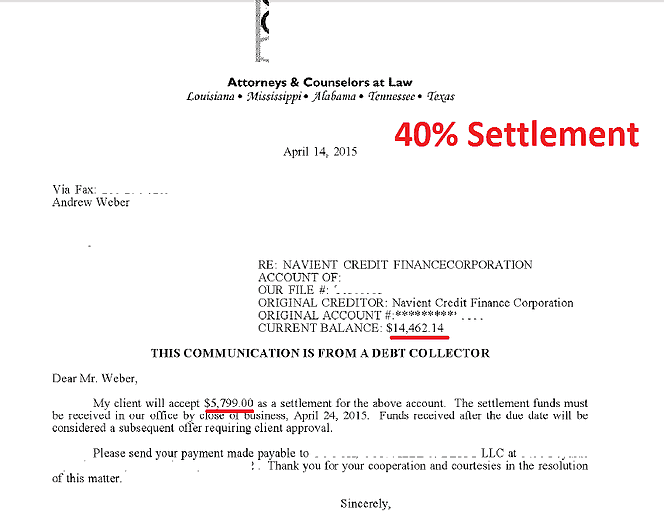

Like this settlement:

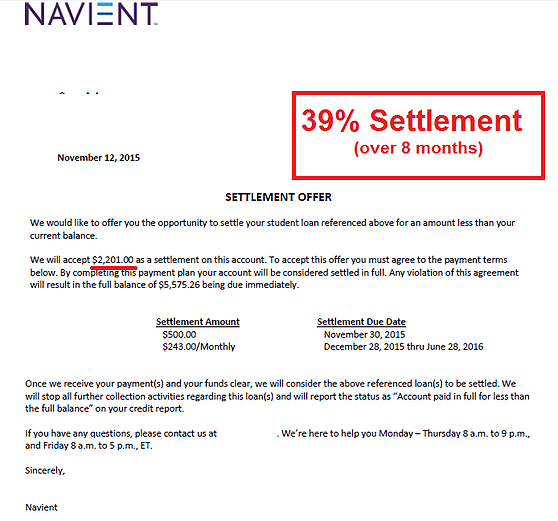

Or this one:

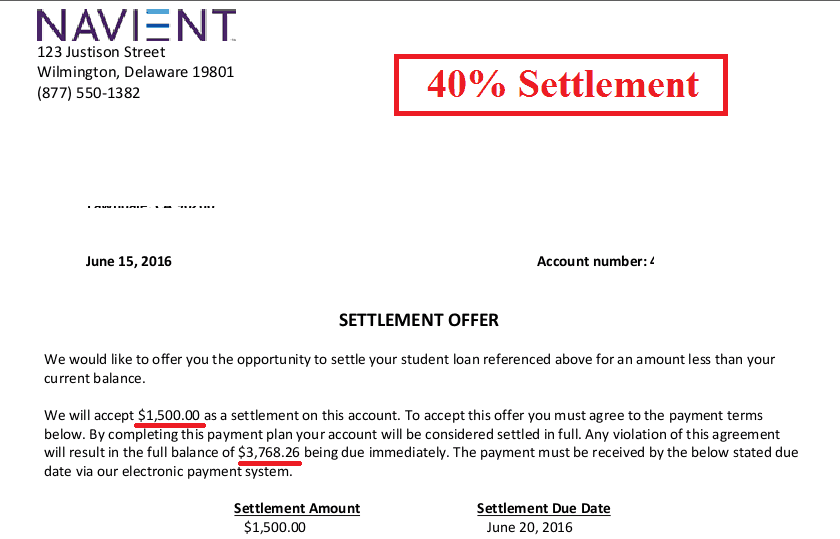

Or this one, which I actually finalized yesterday:

After doing so many Navient settlements, I am confident in my ability to settle recent charge-offs for between 40-45% of the balance.

So let’s crunch some numbers. A 55% settlement of $10,442 means that the balance was about $18,985. A 40% settlement on that same balance would have resulted in a settlement of $7,594. My negotiation charge at 15% of the amount saved (since this account is less than $50,000) would have been about $1708.

The amount of my projected settlement plus my negotiation charge would have been less than what the borrower is paying on the settlement they negotiated – it would be a total of $9,302, which is a difference of $1140 compared to the 55% offer they accepted. That’s a significant amount of money to leave on the table. Avid readers of this blog know I like to often say that “Executing a settlement is just as important as negotiating the dollar amount”. So in addition to paying $1140 more than what my total negotiation charge plus the settlement amount would have been, this person is confused by their settlement letter and does not know how to properly execute the settlement.

They probably don’t know that it’s also a good idea to record a confirmation call with the collector they’ve been working with, or what to say in that call. They don’t have a tried and tested settlement payment protocol that ensures they will have several forms of a paper trail to rely on if there is any issue with the collector after the settlement is paid. They may not know to send a settlement payment by cashier’s check instead of a personal check, how and when to pay a settlement by phone (hint: only with the original lender and only after certain precautions are taken); or what to write in the memo line of a cashier’s check to ensure that the payment can only be applied to the settlement. This individual also didn’t seem to be aware of a specific department at Navient that they could contact to clarify their questions about the account numbers not matching up – where I am on a first-name basis with one of that department’s most helpful agents.

In all fairness, a 55% settlement is decent, and I’m sure the debt collector applied some pressure by saying “it’s only available this month” and “this is the absolute lowest we can go”. I know my friends at that collection agency would never tell a little white lie during a settlement negotiation, would they? (I forgot to mention that I have multiple contacts at the specific collection firm the individual is negotiating with – including a manager). But, for all intents and purposes, this person did all right in their settlement negotiation. The extra 15% of the balance I could have saved them is a solid amount, but not huge. Still, I don’t think anyone would want to give an extra $1100 to a collection agency if they didn’t have to. If their account had been in the high five figures or lower six figures, though, that extra 10-15% of the balance saved (or more) could be a small fortune.

I didn’t propose to take over this borrower’s negotiations to get them a better deal, because the damage is already done – the savvy collection agent already knows the individual has 55% of the balance available based on what they have discussed, and at this point the collection agency won’t accept less when negotiations have progressed to the point of the individual verbally accepting the offer and confirming they have the full amount of funds the collector is asking for.

Settlement negotiation works best when I can fully take over negotiations on a borrower’s account before they have provided any financial information or made any offers to a collector or lender – ideally, before they have even talked to them. Not only will I ensure we get the lowest settlement possible, but I will take all the necessary steps along the way to make sure we will be prepared to successfully execute the settlement. When it comes to DIY settlement, sometimes it seems like you can save more by doing it on your own. In some cases that’s probably true, especially compared to “old school” debt settlement companies that charge ridiculous fees like 20% of the debt amount, or 33% of the savings (for example). But for a debt negotiator who charges the lowest negotiation rates in the industry, the negotiation charge plus the amount they negotiate will very often be less than what a borrower can negotiate on their own.

Another form of added value in hiring a professional is the fact that debt collectors do treat professional negotiators differently. It’s something that I always believed, but in a negotiation last month, a collector actually told me, “well, we have more leeway since you’re involved as a third party”. The same types of collection threats that I would literally laugh at can cause someone without settlement negotiation experience to think that they must take the offer that the collector is presenting. Sorting fact from fiction when communicating with debt collectors is just one of the ways a professional negotiator can save you big bucks – in this case study, over $1000 – versus trying it on your own.

(Me after another long day of settlement negotiations)

That’s not even including all the time that’s involved in negotiating and researching how to negotiate. I can read 100 articles about how to ride a bike, but if I’ve never ridden a bike before, there’s a pretty good chance I might crash the first time I try it. There’s no substitute for the experience a professional debt negotiator has, or the negotiating persona that is developed through that experience. The contacts gained over a negotiating career help too – there is a real rapport when I’m working with an agent or supervisor that I have settled with in the past. The same person who might be badgering my client to take out a home equity loan and pay 80% of the balance (true story) before I get involved, changes to “Oh, hey Andrew” when I give them a call. They know from the first phone call that the tactics they tried with the borrower are not going to work, and that I’m going to be friendly with them, but they also have to give me a good deal like the one(s) they’ve given me before.

Final Thoughts

In summary, we can see that there are plenty of reasons to hire a legitimate debt negotiator who charges a low negotiation rate, not the least of which is a lot more money in your pocket than if you attempt to negotiate on your own. If you have a private student loan you want to settle, contact my office today to see how we can add you to our long list of success stories.