Student loan debt forgiveness is the ultimate ideal outcome for all student loan borrowers, but remains out of the reach of all but a very few – and Navient Student Loan forgiveness is no exception. If you’re interested in going down the route of a forgiveness program for Navient Student Loan, keep reading.

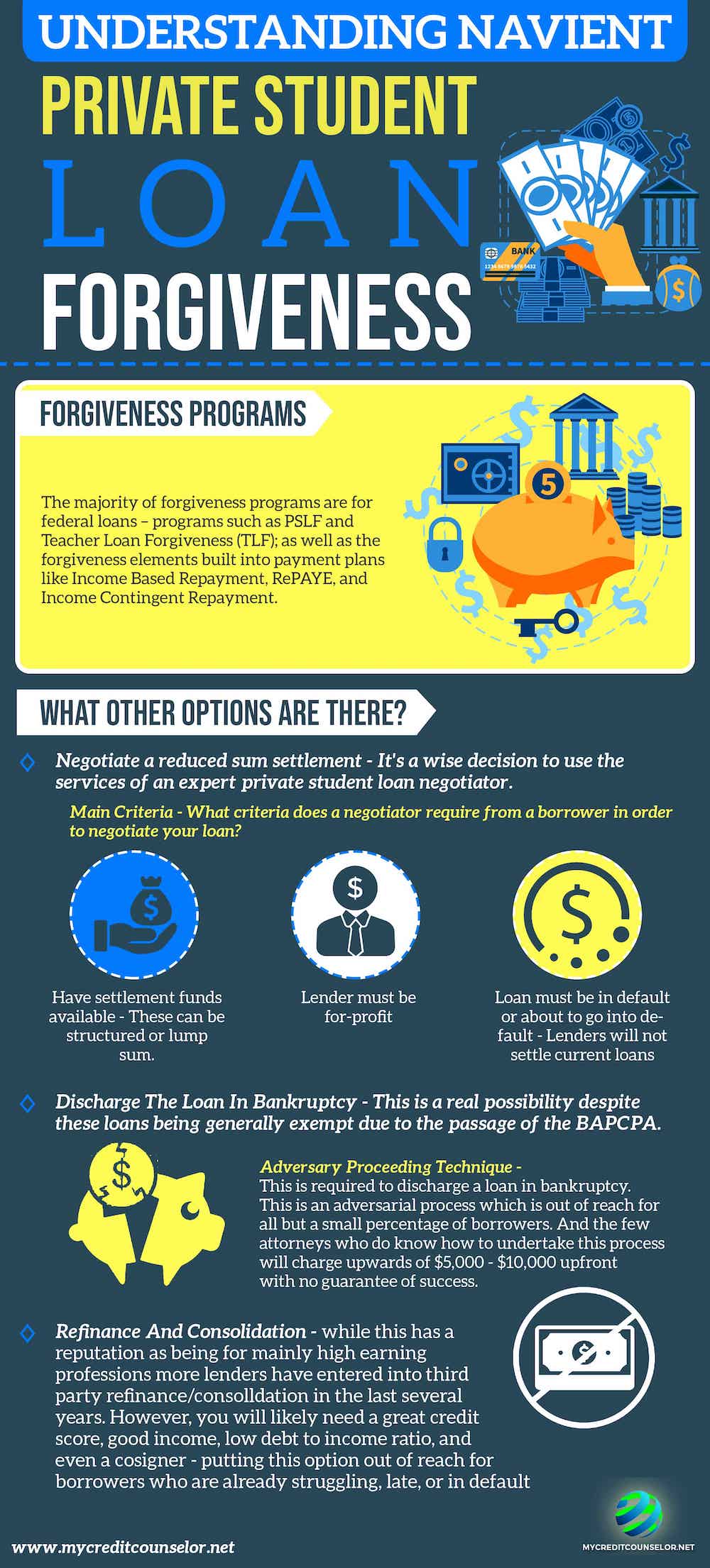

The majority of forgiveness programs (Like what is available in Navient Student Loan) are for federal loans – programs such as PSLF and Teacher Loan Forgiveness (TLF); as well as the forgiveness elements built into payment plans like Income Based Repayment, RePAYE, and Income Contingent Repayment.

There are a multitude of other state and vocation-related forgiveness programs, but there isn’t any specific private loan forgiveness program for students.

The closest thing for most borrowers is the negotiation of reduced sum settlements. Through the skillful negotiation and execution of settlement agreements, loan borrowers can remove the seemingly existential burden of a high balance loan and all of the negative consequences they can carry.

Private loans for students are a truly unique financial product. Generally exempt from bankruptcy due to the BAPCPA passed in 2005, student loans originated by private lenders have more protections for lenders and less payment plans for borrowers than other types of unsecured debt.

Over half of the cosigners who completed a 2017 survey said that their credit scores had declined. This is one of the most common problems I hear about from borrowers who have cosigned.

Any late payments or missed payments by the borrower will result in the cosigner also incurring credit damage.

These types of loans are often taken out by cosigners and borrowers who aren’t fully aware of the difficulty of repaying these loans; or the limited repayment choices and general aggressiveness of the lenders from whom they are borrowing.

The smallest private loan for students experiencing litigation I have heard about was only $4,000; while larger loans over $50,000-$100,000 are almost certain to experience litigation at some point in the collection cycle without pre-emptive action; unless by sheer luck the borrowers have managed to get loans from one of the few relatively non-aggressive lenders who originate private education loans.

Does Navient Offer Forgiveness for Navient Student Loan?

This type of loan settlement experience, namely, Navient student loan forgiveness, can depend a great deal on an individual lender’s policies.

For Navient Student Loan borrowers seeking a forgiveness program via settlement, they will have to contend with very aggressive and savvy collection agents both before and after the default occurs.

Those students who have taken out Navient Student Loan will very likely find that Navient can also be one of the more aggressive lenders (for their Navient Student Loan) when it comes to legal action.

Occasionally with larger accounts of Navient Student Loan, they can go directly to a collection law firm licensed in the client’s state.

The collectors of Navient Student Loan working at these types of law firms are fully aware of the fear and anxiety they can invoke by being employees of a collection law firm, and they use this to their full advantage.

If you have existing Navient Student Loan accounts and you are having time to settle it, then forgiveness from this Navient Student Loan is another option.

Do Any Other Lenders Offer Forgiveness Programs?

Sallie Mae

For those who want to pursue Sallie Mae by settlement, there are many similarities to Navient Student Loan (since Navient split off from Sallie Mae in 2014), but also some behaviors and policies specific to “SLM”; which is now an FDIC insured bank.

National Collegiate Trust

Other lenders like the National Collegiate Trust have developed an aggressive reputation, even though the “NCT” loses many cases when they are challenged by competent attorneys.

Discover

Discover loans are often handled by some very polite yet very difficult collection negotiators in their internal collection department in Salt Lake City, UT; while Keybank and Wells Fargo are also commonly handled by internal collection departments in addition to third party agencies.

Chase

Chase is rumored (for student who fails to pay for their Navient Student Loan), to halted all collection lawsuits for it’s student loan portfolio, while they are no longer originating new loans and have sold some of their portfolios to the National Collegiate Trust; as well as to Navient Student Loan.

Citibank

Citibank employs tough third party debt collectors, but will settle their loans (like Navient Student Loan) in a similar range as their credit card debt with skilled negotiations. There’s no substitute for the experience a professional brings to the negotiating table, or the confidence that experience instills.

Understanding the Ins And Outs

Knowing the ins and outs of how to communicate with each lender, and how to time negotiations to get the best possible deal while reducing the risk of more aggressive collection activity, is central to finding success in dealing with potentially hostile collection agencies and internal departments.

Although there aren’t any specific student forgiveness programs for loans (like for those who avails Navient Student Loan) that are private, the possibility to discharge this type of loan in bankruptcy is real – even with these loans being generally exempt due to the passage of the BAPCPA.

There are several notable circumstances, such as the involvement of a non-accredited university, or the use of funds for non-education related expenses, that can increase the chances of a loan being discharged in bankruptcy.

Although there have been multiple encouraging cases, this is still a very uphill battle that requires an attorney who is experienced in filing Adversary Proceedings against private lenders (and winning).

Adversary Proceeding And Bankruptcy

This “Adversary Proceeding” technique is required to discharge a loan in bankruptcy. There are not very many attorneys who have experience in discharging private loans for students through the use of an “AP”, although this area of the legal profession is attracting more and more attention.

Most lawyers that I have talked to who are experienced in this realm of bankruptcy will charge anywhere from $5,000-$10,000 or more as a legal retainer to do the “AP”, without any guarantee that the “AP” will be successful.

An Adversary Proceeding, as the name suggests, is a very adversarial process which is basically a lawsuit against the private lender. The best attorneys will not attempt an “AP” that they don’t think has a good chance of winning.

According to a study in the American Bankruptcy Law Journal (although 7 years old), only a tenth of a percent of bankruptcy applicants attempt to discharge their student loans. I would assume this number has grown, but has still not come close to a mainstream solution for the majority of private loan borrowers (or federal borrowers, for that matter).

With bankruptcy being out of realistic reach for all but a small percentage of borrowers; the options left are few.

Even without attempting a discharge, a borrower can include a private loan in a CH13 bankruptcy to essentially put it on hold – the lender will not be able to take collection actions, but the loan will not be discharged (without a successful “AP”) and will continue to accrue interest while the CH13 is in place.

This is nothing more than kicking the can down the road, unless the CH13 can be structured in a way that the loan receives no payments and the statute of limitations are not delayed by the bankruptcy.

That type of strategy could potentially run the loans past statutes of limitation, but is easier said than done and varies greatly depending on state law (I can’t provide legal advice, state-specific or otherwise: for SOL questions please contact a knowledgeable attorney in your state).

Payment plans are generally limited or non-existent for private loans. Because these loans are credit based, the lenders do a pretty good job of screening for borrowers and cosigners who have income or assets to repay the loans (at least on paper, at the time the loans are originated).

Therefore, any loan repayment plans are usually in the lenders benefit – whether it’s a forbearance, or a “low interest payment plan” that serves to only help the borrower tread water and nothing more.

Refinance And Loan Consolidation

Refinance and private loan consolidation also seem appealing, and many companies offer refinance of private (and federal) loans for applicants who meet their criteria. However, their selection criteria has been rightly criticized as only accepting “doctors and lawyers”.

While loan refinance is, in theory, open to others outside of those professions; borrowers without great credit, Debt To Income ratios, and high income levels will have a hard time qualifying for a refinance.

Those borrowers who have already fallen behind or defaulted on their loans will likely find refinance to be impossible to be approved for.

Settlement Negotiation

This leaves settlement negotiation as the remaining available option for this type of borrowing. Despite some variables, and a few lenders who try to refuse settlement at reasonable percentages reflective of the industry as a whole (ahem – Discover and PNC, I’m talking to you); settlement is the closest thing to actual forgiveness for borrowers who can afford it.

Having a lender that is a large for-profit company or bank and a legitimate financial, medical, or other hardship exponentially increases the possibility of settlement (as long as settlement funds are available).

The types of settlements possible vary depending on the lender, the hardship, a lump sum versus structured settlement, the date that the account defaulted, the skill and experience of the negotiator, and other circumstances.

Generally, anything at 50-60% of the balance or less is considered a good settlement, although some settlements can be half of that amount.

It’s also important to keep in mind that loan lenders will only agree to good settlements after a significant amount of negotiation in most cases, and always after the loan has defaulted and become a business loss for the lender.

Once the loan becomes “charged off”, the lender still has the right to collect on it for a period of time, but the fact that it has become a nonperforming asset can give the lender the incentive to accept a significantly lower amount than the balance due.

The Forgiven Amount

In fact, lenders even refer to the amount canceled in a settlement as the “forgiven amount”. While taxes may need to be paid on the amount canceled in settlement if the borrower is financially solvent, many borrowers who have more debts than assets at the time of settlement can benefit from the insolvency exception to taxes on cancelled debt.

When carrying out your research on repayment options, for example Navient student loan forgiveness programs, the amount of resources and competing blog articles can be mind boggling.

However, after a careful evaluation of all of the existing options, many borrowers (like those who avails Navient Student Loan) come to the conclusion that loan settlement is the fastest and least expensive way to get rid of a private loan (an opinion with which I agree).

However, this doesn’t mean that it’s right for everyone; although my clients come from all different types of backgrounds, financial and otherwise. In my evaluations, I take an in depth look at a borrower’s financial and personal circumstances to see if settlement is a good option.

There are three main criteria that must align to become a settlement client. 1 – There must be settlement funds available (structured or lump sum). 2 – The lender must be a for-profit student loan lender (like Navient Student Loan) (some nonprofits settle, but not many). 3 – The loans must be in default or will eventually reach default (lenders will not settle current loans).

If these criteria are met, then the possibility for Navient student loan forgiveness to become a reality through settlement is very real.

You can read up our ultimate guide to private student loan forgiveness here.