After a tumultuous 2020, the likelihood that Joe Biden will be inaugurated in January is no longer a question, and student loan borrowers are wondering what impact this will have on them. There are a wide variety of blogs and articles that have been published recently about student debtors, and the hopes that a president elect Joe Biden will throw them a lifeline; but most of these articles deal with federal loan provisions ranging from potential cancellation, to an extension of the Cares Act. None have yet discussed the specific impact a Biden administration will have on bank backed, non-federal student debt including a possible Joe Biden private student loan forgiveness program.

I’ve been hearing more questions about this within my practice in recent months, with some clients and potential clients asking me if their loans from non-federal lenders will be canceled or forgiven. At the same time, there has been a lot of talk and speculation about federal student loan forgiveness, with Biden’s campaign being supportive of a $10,000 or larger amount canceled per borrower (although implementation would be complex, it appears that there is legal precedent to support unilateral federal loan actions through executive order).

For private borrowers, there has been very little said, and so far, no experts have chimed in to give their opinion – until now. Non-federal loan borrowers unfortunately seem to be an afterthought, but every week, I hear from people who tell me: “I have my federal loans under control – the repayment plans are flexible. But it’s these bank originated loans that I’m struggling with”. I hear this refrain over and over.

So, will the Biden administration take definitive action to cancel private student loans?

This (politically neutral) article will go into detail on what would be necessary for that to happen; and will evaluate the likelihood of it taking place.

No mechanism exists for a president to wave a wand and cancel private debt without going through Congress.

Spoiler alert: I strongly believe that there will not be any type of blanket forgiveness for privately backed loans. The executive branch simply doesn’t have the authority to do anything like that unilaterally with an executive order; any more than they would have the ability to write an executive order that cancels payday loan debt or credit card debt.

It would have to go through Congress, and it would be classified as a bailout – taxpayer money sent to private lenders to wipe out their existing balances. Congress will either be divided, or if the Democratic Party wins both runoff races for the Senate in January; it will be in Democratic control but without a filibuster-proof majority. The political headwinds are the main reason that this will not even get off the ground, but looking at how a potential process would work shows that it would be very difficult to implement.

While this type of action would no doubt have a massive positive impact on borrowers with bank-originated student loans themselves, a $130 billion payoff would also be extremely beneficial to the lenders, who would just turn around and originate more privately backed loans next year (since the root cause – tuition costs – will still be there). For that reason it would be looked at as a major bailout of an unpopular industry, for which there is little political appetite after the bailout of the “too big to fail” banks and financial institutions during the Great Recession.

What would be the impact of forgiveness/cancellation for the private loan industry?

When these lenders sell their portfolios to each other, or to debt buyers, it is for less than the face value of the loans. However, if all loans were paid off in full, it would be a huge boon to these lenders.

How do large institutions react when they receive bailouts? We only have to look back to the Great Recession to see that they use them to line their own pockets, buy back stocks, and many other steps that serve to help them first, with the borrowers a secondary and minor consideration. If collegiate loans from banks were somehow given blanket forgiveness, it would be in the form of writing a check directly to the lenders for the open balances they have on their books, and any defaulted debt.

What would these lenders do? They would take this massive financial windfall and turn around to originate even more loans the following year.

Why? Because the root cause of the reason for the existence of this type of loan is not going to go away by paying off the existing outstanding ledger.

Demand for private loans will not go away even if the total outstanding balance is canceled.

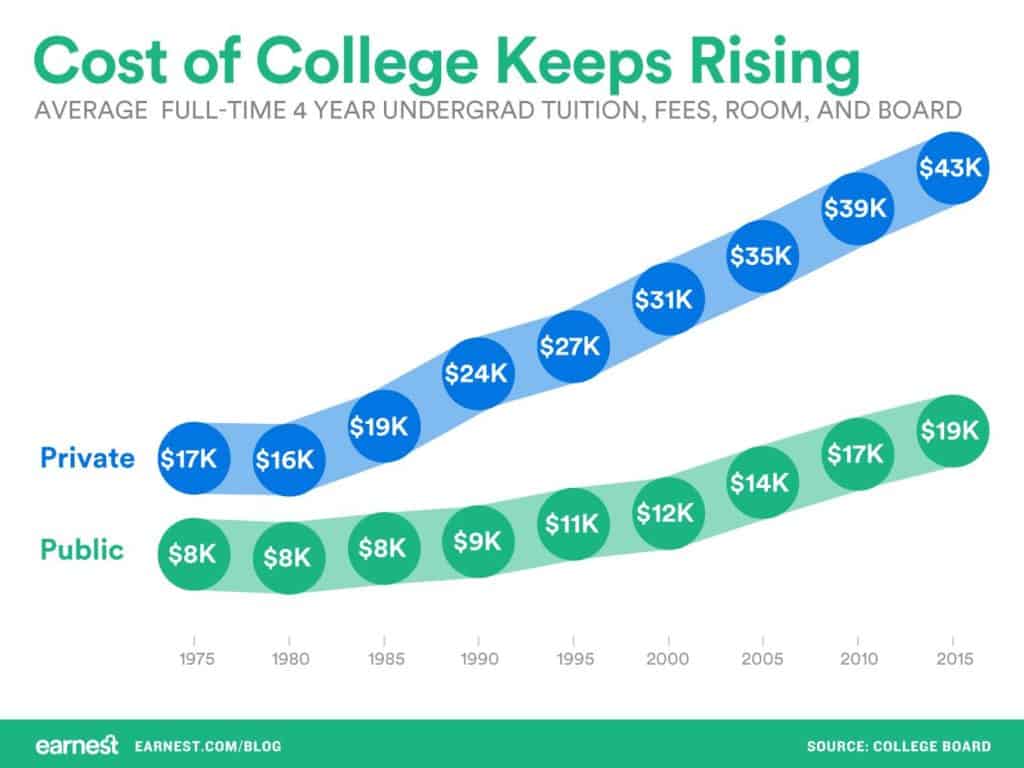

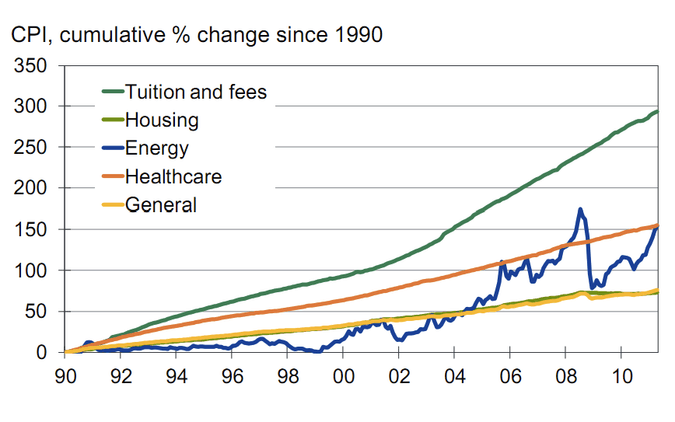

Bank-backed student funding is used as a supplemental means to fund various types of college, university, and secondary school tuition; and makes up 2-3% of overall higher education spending each year. We have not taken steps to make college more affordable, which could eliminate the need for some loans. It’s hard to see how the need for them would be completely eliminated unless the United States moves towards a full European style higher education system, which does not seem possible anytime soon.

Free community college is something that has been advocated for, although this will also be very difficult to achieve with the current political climate. Most of the private borrowers I talk to have taken out their loans for other types of schooling though – whether it’s a state university, private university, art, technical, aviation, law or medical school. So even if community college is made available tuition free, this will likely have a very minimal impact on the demand for loans that are private.

If private student lenders will turn around and originate billions of loans after they receive a payoff of their current portfolios, will it be politically feasible for any administration to basically write these lenders a $130 billion check even if it is able to be ratified by both houses of Congress? Would it even solve the problem of why we have privately backed loans in the first place?

No. All this would do would be to help out the current group of private student loan borrowers (and it would help them greatly), but it would not be any type of long term solution to the private student loan problem in the first place.

Would another bailout check be issued by the government next year for the next set of loans that are originated after the first set of forgiven private loans? And the year after that? By taking a hard look at exactly how forgiveness for privately backed loans would play out and what technical processes would be involved, as well as how it would impact the overall industry, we can see how difficult it would be for any president to make this a reality; even if their party was in full control of Congress.

For ongoing forgiveness year after year, it would essentially have to be a 100% government subsidized industry, and there is little political appetite for that on either side of the aisle. While there are those who think that all education spending should be through the government, and also those who think that all student lending should be through the private market; there is no one seriously advocating for all private lenders to be fully funded by federal subsidy. We already had a system like this with FFELP federal loans, which was dismantled in 2010 as a wasteful and inefficient system that mainly benefited the lenders and servicers who handled the federally backed government loans.

There are other concerns too – many private lenders also offer refinance, which converts federal loans into bank originated loans with a lower interest rate (but less federal borrower protections). If it looked like there was going to be blanket forgiveness for privately backed loans coming, many federal loan borrowers would no doubt rush to refinance in order to convert their loans into bank originated loans, which could massively increase the cost of the bailout.

The higher education industrial complex has a powerful lobby and a great deal of political and financial strength – which is firmly invested in keeping the industry the way that it is. Private lending is a growing industry, and with the addition of refinance lenders in the last decade, is poised for further growth as they meet a need for supplemental tuition funding; fueled by the spiraling cost of higher education for both public and private universities.

What about bankruptcy?

Currently, it’s very difficult to discharge a private or federal student loan in bankruptcy; and requires a skilled bankruptcy attorney who is familiar with the Adversary Proceeding process, and an applicant who has to jump through a series of very difficult hurdles to qualify. While it is possible, this is not currently a form of relief open to most borrowers.

Bankruptcy laws may be reformed to allow the addition of bank backed college funding without an Adversary Proceeding, but even then, most people will qualify only for a Chapter 13 partial repayment bankruptcy, and not the Chapter 7 total liquidation bankruptcy. But bankruptcy is no walk in the park, even without having to file an Adversary Proceeding – it can involve surrendering assets, closing credit cards, and tanking your credit for quite a long time. However, it would provide some relief to some of the worst off borrowers with a bank originated loan if the 2005 BAPCPA (which incidentally, Biden was involved with as a Senator) was relaxed to include student loan borrowers.

The closest thing to a loan forgiveness program for privately funded student debt that currently exists, is settlement.

While it is unlikely that any government action is going to result in the widespread cancellation of privately held student loans, it doesn’t mean that you can’t still wipe them out and move on with your life. I specialize in settling private student loans, and through a combination of over a decade of experience, high level strategy, and ongoing negotiating relationships with lenders and collectors; I’m able to settle bank originated loans for far less than the amount owed. If you want to see if I’m able to help you settle your private student loans like I have for hundreds of other borrowers and cosigners, give me a call today, or fill out my evaluation form so that I have a full picture of your situation.